Get Ready to Pay More for Homeowner's Insurance.

I started drafting this letter when I discovered that CA Fair Plan insurance rates were going to explode higher this fall. My first thought was, “Our clients on Fair Plan need to know this in advance”. In the past 10 days or so, I’ve done a lot more reading about homeowners insurance availability in California. I’ve spoken with experts. Homeowners insurance in California is a hot mess, and it’s probably going to get more complicated and more expensive. By the time I went back to drafting I’d come to the conclusion that I would never want to purchase homeowners insurance in California without the help of a veteran, qualified specialist. There is just too much to know, and too many potential mistakes that can be made. The purpose of insurance is to protect you from financial disaster. Most people find out what their insurance doesn’t cover the moment they need that coverage. So before I go any further I want to give you the names of some highly qualified people who specialize in providing this coverage.

Chuck Reyna is a veteran of these crazy markets. He’s with Aon Private Risk Management in San Francisco, CA. His email address is Chuck.reyna@aon.com. His cell phone number is 925-437-4104.

Jennifer Thompson and Gannon Laidlaw are with Jaffe Insurance Agency, an independent insurance agency with offices in Marina Del Ray and Napa, CA. Her email address is Jennifer@JaffeInsurance.com. Her cell phone number is 310-827-6186. Gannon focuses on new business placement and works with clients on homeowners, auto, umbrella, landlord, and commercial insurance needs. His email address is Gannon@JaffeInsurance.com. His cell phone number is 707-337-2473.

Both Aon and Jaffe insure homes all over the state of CA. They insure homes of 5T’s clients. They both have extensive experience dealing with the biggest risks we face right now, fire and water damage. Chuck, Jennifer and Gannon care, and they are easy to talk with!

The San Francisco Chronicle recently reported that “California homeowners relying on the states Fair Plan insurance will soon face the largest premium hike in years, with rates set to rise nearly 30% on average in October.” In 2021 FAIR plan covered only 242,000 homes. It covered approximately 684,388 as of March 2026, and the number is growing. That makes them the third largest homeowner insurer in California after State Farm and Farmers Insurance Group, and their premiums are exploding upward.

CA Fair Plan policyholders can expect to see their new premium at their first renewal date following Oct. 15. Megan Fan Munce, staff writer for the Chronicle reports: “The largest component of the increase relates to the wildfire portion of policyholders’ premiums, so those policyholders whose properties are at significant wildfire risk will see a higher increase than those at lower risk, and some policyholders will see a premium decrease, according to a spokesperson for the FAIR Plan.”

This is the first statewide rate increase for the FAIR Plan since 2023, when it raised premiums by 15.7% overall. FAIR stands for Fair Access to Insurance Requirements. The California FAIR Plan is a basic, last-resort fire insurance program designed for homeowners who cannot get coverage from traditional insurers because their property is considered too risky — usually due to wildfire exposure. It is not a full homeowners insurance policy by itself. Most homeowners need to combine it with a supplemental policy called a Difference in Conditions (DIC) policy to get broader protection. Think of the FAIR Plan as “bare-bones fire insurance for properties traditional insurers won’t cover”.

Homeowners in higher fire risk areas should probably expect continued annual premium increases, tighter inspections by insurers, mandatory defensible-space requirements, more non-renewals in high risk fire zones, and greater use of FAIR plan +DIC coverage.

The San Francisco Chronicle reports that private insurers will also be raising rates. Farmers, Mercury, USAA, Pacific Specialty, and California Casualty will all be announcing rate increases before September 15th, 2026. Companies like these operate in the “traditional admitted market” of insurers in California. Given the increasing risks from climate catastrophe, fire and water, two other entitles now act as massive insurers for California. The Fair Plan is one of them and it’s currently the primary option for most homes in heavily forested or high-risk fire zones.

The other is call the surplus lines, or non-admitted market. It includes specialty insurers like Chubb Custom, which dominates the luxury, high value home sector. Other participants in the luxury, high-value sector include PURE, Cincinnati Surplus Home Insurance. Together, these carriers write thousands of customized policies for expensive homes and estates that fall outside standard underwriting guidelines. Because they are not subject to the state’s usual rate-setting rules, they can insure higher-risk properties by pricing coverage to reflect local hazards. Jennifer Thompson told me about a home in Oakville, Napa County, that she insured with $5 million in excess fire coverage. The annual premium for that coverage is $65,000, in addition to a $10,000 California FAIR Plan premium and $5,000 for supplemental insurance, bringing the total annual cost to $80,000.

A newer entrant to insuring high risk homes, with total potential claims of $3 million or less, is Delos Insurance Solutions. Delos was built by aerospace and data scientists specifically to write home insurance in areas exposed to wildfire. They use highly advanced satellite imagery, NASA data, and AI modeling to look at individual properties. They often find that a specific home is actually safe from fire, even if traditional legacy models have blacklisted the entire zip code.

Chuck Reyna, from Aon Private Risk Management, told me about several other newer insurers, including Pacific Coastal, Stand, and Rivington Specialty. They all employ very advanced, sophisticated, proprietary wildfire risk modeling. Rivington is limited to $4m in dwelling coverage, Pacific Coastal can offer up to $10m dwelling coverage, while Stand can accommodate up to $20m in Total Insured Value (the combination of the dwelling, separate structures, personal property, and loss of use limits combined).

The good news is that newer carriers are entering the California market. The bad news is that all insurance is expensive these days. Possibly more important is the fact that coverage offered by the various carriers, admitted and unadmitted, can vary widely. You might have insurance against fire damage, but not water damage, and unless you’ve read the fine print you won’t know until your house floods! Meghan and I have been through that. Having three feet of water in your house is no fun, especially in the dead of winter in Truckee, CA!

It was not my intention to make recommendations or even talk about alternatives to the Fair Plan when I started writing this letter. I simply wanted to make you aware that big premium increases are on the way. They are going to be a real shock for some. But I have come to understand that this market is so complex I would not proceed in it without professional guidance.

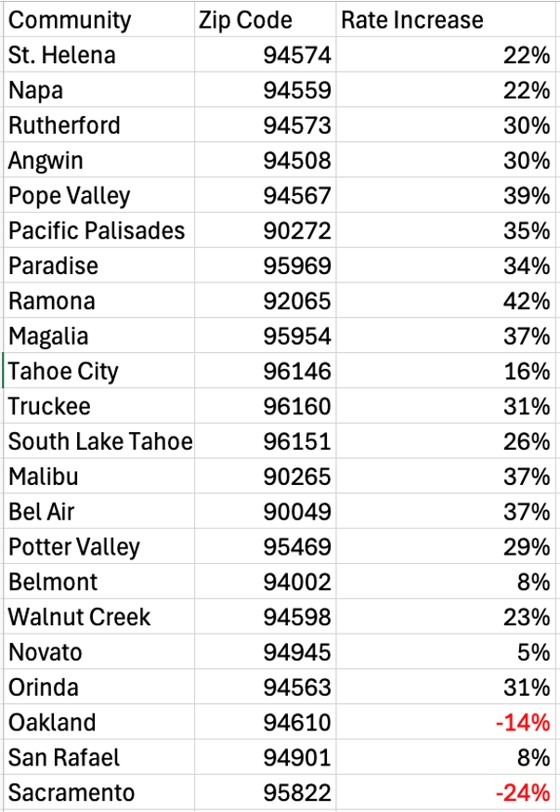

Here is a sampling of the Fair Plan projected rate increases, and two decreases in several communities. The source of these numbers is from an article written by Megan Fan Munce of the San Francisco Chronicle on May 20, 2026. She linked the California Fair Plan website to her article. We have clients living in many of these zip codes. That’s why I selected them to highlight.

Grizzly Flats, CA, in El Dorado County, zip code 95636 will be experiencing the largest rate hike, at 108%! No clients there, but Ouch!

If you are on the CA FAIR PLAN, you might want to check out what options are available to you before those new rates take effect. If you are on any other plan that you put together yourself, I strongly encourage you to call Chuck, Jennifer, or Gannon. Get a second opinion. For the record, we do not share in any of their compensation. Nor do we get referral fees. As I am finishing this newsletter I’m realizing that Meghan and I are now paying more in annual insurance premiums for our two homes than the total cost of my first house!

All the best,

Paul Krsek

CEO

5T Wealth, LLC

Main (707) 224-1340

Cell (707) 486-7333

Paul@5twealth.com

Disclosure and Disclaimer - Updated last on October 14, 2025:

CEO's Corner is a proprietary newsletter written for clients, friends, and affiliates of 5T WEALTH, LLC (5T), which is an SEC registered investment advisor. Information presented is for educational purposes only. The information does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and are not guaranteed. 5T has reasonable belief that this letter does not include any false or material misleading statements or omissions of facts regarding services or investments. 5T has reasonable belief that the content as a whole will not cause an untrue or misleading implication regarding the adviser’s services, investments, or client experiences.

The opinions expressed are those of the author and are subject to change without notice. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Any opinions, projections, or forward-looking statements expressed herein are solely those of the author. They may differ from the views or opinions expressed by other areas of 5T and are only for general informational purposes as of the date indicated.

5T has presented information in a fair and balanced manner. 5T is not giving tax, legal, or accounting advice.

Past performance should not be considered an indicator of potential future performance. If you do not consider yourself suitable, either emotionally or financially, to experience volatility and/or losses in financial markets, you should not invest. The portfolio managers at 5T do not guarantee investment results.

Charts, displays and graphs may be used as illustrations. They are not intended to be used by themselves to determine which securities to buy or sell, or when to buy or sell them. Such charts and graphs offer limited information and can’t be used on their own to make investment decisions.

CEO Corner does not represent the opinions of Fidelity, Fidelity Institutional Brokerage Group, NFS or anyone employed by Fidelity in any capacity. Neither Fidelity, Fidelity Institutional Brokerage Group, nor NFS, nor anyone employed by Fidelity in any capacity has participated in the creation of CEO Corner and they are not responsible for the contents or distribution of CEO Corner.

CEO Corner does not represent the opinions of Charles Schwab Corporation, Schwab Advisor Services or anyone employed by Schwab in any capacity. Neither Charles Schwab Corporation nor Schwab Advisor Services, nor anyone employed by Schwab in any capacity has participated in the creation of CEO Corner and they are not responsible for the contents or distribution of CEO Corner.

The investment objectives of various strategies mentioned in CEO Corner may be substantially different from one another. Therefore topics or investments mentioned in CEO Corner may or may not apply to specific managed accounts and/or strategies. If you are unsure which strategies your accounts are invested in please ask a representative of 5T to clarify that for you.

The assets held in managed accounts at 5T may include stocks, bonds, cash, commodities, foreign exchange, mutual funds or exchange traded funds (ETF's), money market accounts or limited partnerships that represent the same. They are subject to market fluctuation and the potential for losses. The assets are not insured. The value and income produced by these investment products may fluctuate, so that an investor may get back less than they initially invested.