If the Fed can't beat inflation they can always change the way its calculated.

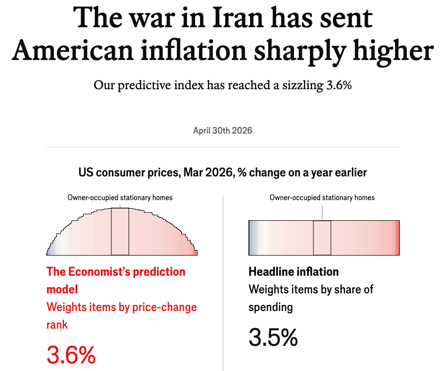

The Fed has been trying to drive “official” inflation down to 2% for years, with no luck so far. Recently “official” inflation has been rising, not falling. The Economist publishes their own inflation gauge. I like it because it’s free of government manipulation. As of April 30, 2026 issue they estimate that “official” inflation is back up to 3.5% to 3.6%.

The Fed, under Chair Powell has used “Core PCE”(Personal Consumption Expenditures) as its official inflation guide. At the end of April it was at 3.2%. Today we got April "Consumer Price Index (CPI). It ran a hot 3.80%.

All of these inflation gauges are well above the Fed’s 2% target. So the new Fed Chair, Kevin Warsh, plans to change to a different gauge. He’s proposed shifting to “Trimmed Mean PCE”, a metric published by the Federal Reserve Bank of Dallas. Guess what?! According to “Trimmed Mean PCE” annual inflation is only 2.3%. How convenient; don’t like the score card, just get out your pencil and change it!

Under the current “Core PCE” gauge, the Fed looks like its failing and can’t cut rates. Under Warsh’s “Trimmed Mean” gauge the Fed is within 0.3 points of its target. The shift can allow Warsh to statistically justify rate cuts without officially admitting he’s tolerating higher inflation. He argues that one-time shocks, like tariffs or geopolitical shifts shouldn’t dictate long-term interest rate policy.

This isn’t the first time the Fed has changed its official gauge. Headline CPI (Consumer Price Index) was used for many years until Alan Greenspan changed to Core CPE in February 2000. Greenspan made the change for the same reason Warsh is changing. Consumer Price Index (CPI) tends to run a little higher than Core CPE. From 1980 through 2024 CPI has been about 0.3 to 0.4% higher than Core CPE. Changing the index instantly "lowered" inflation!

I remember when Greenspan made the change. His rationale made more sense to me at the time than Warsh’s does now. CPI uses a fixed basket of goods. It assumes that if the price of steak goes up, you keep buying steak at higher prices. CPE assumes you might substitute chicken for steak. It captures a shift in behavior that results in a lower overall inflation reading.

Powell tightened up the calculation of Core PCE during his term, creating “Super core PCE”, attempting to make the sources of inflation more identifiable.

Hopefully you are understanding the trend. When the Fed fails to bring inflation down to target, they can just change the way its calculated! The change that Warsh is proposing is the biggest one yet. In my opinion the last true inflation fighter was Paul Volker.

None of these methods tell us how much inflation we actually “feel”. There are over 200 spending categories that make up the Economist’s index of inflation. There are 201 spending categories in Core PCE. There are 211 in CPI. Each method parses the data differently to come up with official inflation. The odds are incredibly small that any of them actually calculate the inflation you “feel”.

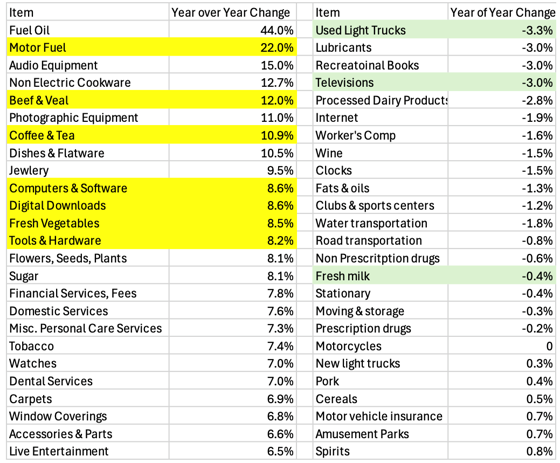

Here’s a table of the 25 categories whose prices increased the most and the 25 that have increased the least from March 2025 through March 2026 in the Economist’s index.

Note that “Used Light Trucks” have decreased in price. I’ve never purchased a used light truck, but I fill the gas tank of the truck I own regularly. I haven’t purchased a television in years, but I buy beef, coffee, tea, and fresh vegetables regularly. I haven’t purchased fresh milk in years, but I buy computers, software, apps, and tools fairly regularly. I’m sure you get my point.

For many of us, maybe most of us, the amount of inflation we feel is much higher than “official” inflation.

While “official” inflation also says wages are keeping up, many households are falling behind because of the costs of non-discretionary essentials have outpaced the general index. In 2016, a $500,000 home mortgage at 3.5% interest cost roughly $2245.00 per month. In 2026, even a good rate of 6.3% on that same loan costs $3095 per month. This extra $10,000+ per year in interest expense is a massive drain on disposable income not fully reflected in wage statistics.

The median cost of home prices and rents have significantly outpaced “official inflation since 2016. Insurance premiums, home and auto, are up 20-40% in many regions over the last two years alone.

The cost of servicing credit cards and mortgage debt is at a 20 year high. This cost is not fully captured in “official” inflation but deeply felt in disposable income.

I’m very concerned about these trends. We’re witnessing the most extreme divide between “haves” and “have nots” in a very long time. Certainly as far back as the beginning of the 20th century, before labor unions were formed. the situation continues to worsen.

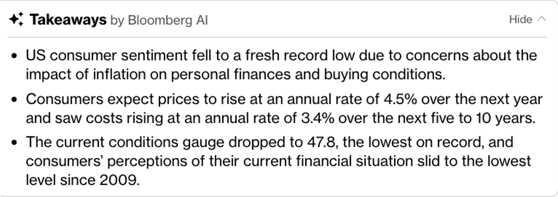

Check out these headlines from Bloomberg.com on May 8, 2026:

The odds of short term interest rate cuts have increased since Warsh announced his desire to make this change. The odds have also increased that we’ll see more inflation, not less. The biggest critique of the “Trimmed Mean” is that it is mathematically designed to ignore real current economic conditions.

The Tariff Problem: If new tariffs cause a sharp 15% spike in the price of imported goods (steel, electronics, etc.), the Trimmed Mean will see that spike as an "outlier" and throw it out.

The Energy Problem: Similarly, if the conflict in Iran keeps oil prices structurally higher, the Trimmed Mean will "trim" those gains.

The Result: The index will report that inflation is "near 2%," while actual cost of living is rising by 4% or 5%. If Warsh changes the gauge and then cuts rates based on that 2% number, he could accidentally pour gasoline on an already-burning fire.

All the best,

Paul Krsek

CEO

5T Wealth, LLC

Main (707) 224-1340

Cell (707) 486-7333

Paul@5twealth.com

Disclosure and Disclaimer - Updated last on October 14, 2025:

CEO's Corner is a proprietary newsletter written for clients, friends, and affiliates of 5T WEALTH, LLC (5T), which is an SEC registered investment advisor. Information presented is for educational purposes only. The information does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and are not guaranteed. 5T has reasonable belief that this letter does not include any false or material misleading statements or omissions of facts regarding services or investments. 5T has reasonable belief that the content as a whole will not cause an untrue or misleading implication regarding the adviser’s services, investments, or client experiences.

The opinions expressed are those of the author and are subject to change without notice. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Any opinions, projections, or forward-looking statements expressed herein are solely those of the author. They may differ from the views or opinions expressed by other areas of 5T and are only for general informational purposes as of the date indicated.

5T has presented information in a fair and balanced manner. 5T is not giving tax, legal, or accounting advice.

Past performance should not be considered an indicator of potential future performance. If you do not consider yourself suitable, either emotionally or financially, to experience volatility and/or losses in financial markets, you should not invest. The portfolio managers at 5T do not guarantee investment results.

Charts, displays and graphs may be used as illustrations. They are not intended to be used by themselves to determine which securities to buy or sell, or when to buy or sell them. Such charts and graphs offer limited information and can’t be used on their own to make investment decisions.

CEO Corner does not represent the opinions of Fidelity, Fidelity Institutional Brokerage Group, NFS or anyone employed by Fidelity in any capacity. Neither Fidelity, Fidelity Institutional Brokerage Group, nor NFS, nor anyone employed by Fidelity in any capacity has participated in the creation of CEO Corner and they are not responsible for the contents or distribution of CEO Corner.

CEO Corner does not represent the opinions of Charles Schwab Corporation, Schwab Advisor Services or anyone employed by Schwab in any capacity. Neither Charles Schwab Corporation nor Schwab Advisor Services, nor anyone employed by Schwab in any capacity has participated in the creation of CEO Corner and they are not responsible for the contents or distribution of CEO Corner.

The investment objectives of various strategies mentioned in CEO Corner may be substantially different from one another. Therefore topics or investments mentioned in CEO Corner may or may not apply to specific managed accounts and/or strategies. If you are unsure which strategies your accounts are invested in please ask a representative of 5T to clarify that for you.

The assets held in managed accounts at 5T may include stocks, bonds, cash, commodities, foreign exchange, mutual funds or exchange traded funds (ETF's), money market accounts or limited partnerships that represent the same. They are subject to market fluctuation and the potential for losses. The assets are not insured. The value and income produced by these investment products may fluctuate, so that an investor may get back less than they initially invested.