The Wealth Divide Gets Wider

On Thursday June 11th, the whole world fixated on Elon Musk becoming the world’s first trillionaire. A trillion is 1000 times larger than a billion and 1,000,000 times larger than a million. One million seconds is equal to about 11.5 days. One billion seconds is equal to about 31.7 years. One trillion seconds is equal to about 31,688 years, which would take us back to the Upper Paleolithic ice age, long before civilization began. Good for Elon!

Lots of other people made great money from Space X, and good for them too! I found this image online, and thought it was pretty funny, but it also makes a point.

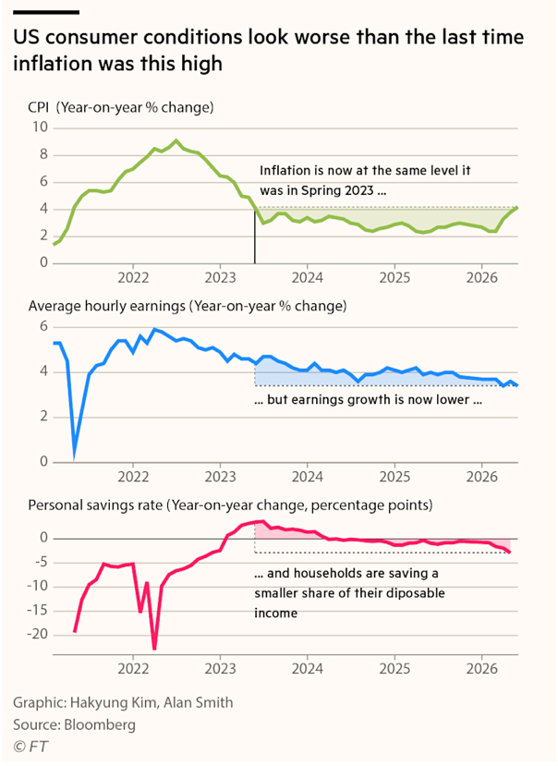

I wrote a newsletter on April 24th in which I said, “I consider myself fortunate to be an investor, and therefore able to increase my wealth by making money work harder rather than Meghan and me working harder. There are many families in this country that can’t do that.” Families that can’t invest, and even small investors, are really feeling pinched. The same day that Space X when public this appeared in Financial Times.

It could hardly be worse for wage earners these days. Headline inflation is the highest it’s been since 2023, wage increases are slowing, and personal savings has gone negative.

The articles authors were quick to point out that while “headline” inflation is back above 4.2%, “core” inflation (which strips out volatile food and energy prices) came in at a “much more tame 2.9%.” While statistically accurate, this “logic”, if you can call it that, always frustrates the H--- out of me. What are we spending the most on, day after day? Food and energy, right?! When inflation actually gets back below 3% I’ll be less angry. In the meantime, don’t ignore that people are being squeezed.

Average hourly earnings spiked after covid and have been steadily declining since 2022. Personal savings rate has been declining for three years. The authors state, “the declining annual level of personal savings rate indicates households are sustaining spending by saving less or drawing down savings.” As if that’s a good thing?! All the while the stock market keeps “whistling a happy tune”, and the financial divide keeps getting wider.

It begs the question, how many people are actually participating in the buildup of wealth accruing from rising stock prices? Approximately 12.5% of American households have a net worth of $1 million or more, excluding their primary home equity. This jumps to 18.5% when primary home equity is included in net worth. Interestingly, according to the Federal Reserve, only 54.3% of Americans hold any form of retirement account at all. That means that 45.7% have no retirement savings. These people handle emergencies by taking on credit card debt, borrowing from friends or family or just cutting back on expenses. They make the choice of whether to eat or pay rent. Before we brush past these numbers, let it sink in that almost half our population has no retirement savings.

I’ve always understood that “figures lie and liars figure”! It’s so true, so often. I bring it up in this context only because it is hard to get your head around all the combinations of numbers that appear in studies on who has enough retirement savings and how doesn’t. But I’ll narrow it down for you. In the 65-74 age bracket the “median” household net worth is $410,000. That represents the exact middle household. The “average” net worth is over 1.5 million. The “average” is heavily skewed upward by ultra-high net worth households in the top percentile of the population in the age group. What’s the punch line? Most households in their “peak years” are worth less than $1 million. One million doesn’t go very far in retirement these days.

And what about Social Security? Without an emergency rescue by Congress benefits will likely be cut by about 20% by 2032. That’s only six years away. Last Thursday I spoke with a person, mid-70’s in age, who is now living on Social Security and a $500,000 investment portfolio. It’s doable. Many live on a lot less. But it’s not fun and its worrisome.

I’m making a simple point here, and it’s the same one I made in April. The few in our society are getting wealthier than ever. The many in our society are not. This is not going to work forever. I can see political and social unrest rising in the future. I can see more and more “senior citizens” struggling to make ends meet. I can see families challenged by taking care of parents at the same time they are trying to raise children.

I don’t begrudge Elon Musk $1 trillion. I really don’t. I sure as heck don’t begrudge Meghan and me for working as hard as we have all our lives, and being among the fortunate few, even though we don’t have $1 trillion. 😂 But I worry a lot about the society we’ve become, and the many that are falling farther and farther behind. I worry what will become of all of us if we don't fix this problem.

All the best,

Paul Krsek

CEO

5T Wealth, LLC

Main (707) 224-1340

Cell (707) 486-7333

Paul@5twealth.com

Disclosure and Disclaimer - Updated last on October 14, 2025:

CEO's Corner is a proprietary newsletter written for clients, friends, and affiliates of 5T WEALTH, LLC (5T), which is an SEC registered investment advisor. Information presented is for educational purposes only. The information does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and are not guaranteed. 5T has reasonable belief that this letter does not include any false or material misleading statements or omissions of facts regarding services or investments. 5T has reasonable belief that the content as a whole will not cause an untrue or misleading implication regarding the adviser’s services, investments, or client experiences.

The opinions expressed are those of the author and are subject to change without notice. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Any opinions, projections, or forward-looking statements expressed herein are solely those of the author. They may differ from the views or opinions expressed by other areas of 5T and are only for general informational purposes as of the date indicated.

5T has presented information in a fair and balanced manner. 5T is not giving tax, legal, or accounting advice.

Past performance should not be considered an indicator of potential future performance. If you do not consider yourself suitable, either emotionally or financially, to experience volatility and/or losses in financial markets, you should not invest. The portfolio managers at 5T do not guarantee investment results.

Charts, displays and graphs may be used as illustrations. They are not intended to be used by themselves to determine which securities to buy or sell, or when to buy or sell them. Such charts and graphs offer limited information and can’t be used on their own to make investment decisions.

CEO Corner does not represent the opinions of Fidelity, Fidelity Institutional Brokerage Group, NFS or anyone employed by Fidelity in any capacity. Neither Fidelity, Fidelity Institutional Brokerage Group, nor NFS, nor anyone employed by Fidelity in any capacity has participated in the creation of CEO Corner and they are not responsible for the contents or distribution of CEO Corner.

CEO Corner does not represent the opinions of Charles Schwab Corporation, Schwab Advisor Services or anyone employed by Schwab in any capacity. Neither Charles Schwab Corporation nor Schwab Advisor Services, nor anyone employed by Schwab in any capacity has participated in the creation of CEO Corner and they are not responsible for the contents or distribution of CEO Corner.

The investment objectives of various strategies mentioned in CEO Corner may be substantially different from one another. Therefore topics or investments mentioned in CEO Corner may or may not apply to specific managed accounts and/or strategies. If you are unsure which strategies your accounts are invested in please ask a representative of 5T to clarify that for you.

The assets held in managed accounts at 5T may include stocks, bonds, cash, commodities, foreign exchange, mutual funds or exchange traded funds (ETF's), money market accounts or limited partnerships that represent the same. They are subject to market fluctuation and the potential for losses. The assets are not insured. The value and income produced by these investment products may fluctuate, so that an investor may get back less than they initially invested.