Understanding Last Week's Jobs Report

Last Friday was an unusual day for domestic stock prices as almost every major stock index finished down over 2% for the week. This was the first sharp correction since the middle of April. Many International stock indexes fared worse, on the back of some unfavorable news regarding Trump’s tariff deals, or lack thereof. For domestic stocks, the vast majority of Friday’s damage came after a disappointing jobs report. It didn’t help that Trump immediately moved to kill the messenger by firing Erika McEntarfer, the head of Bureau of Labor and Statistics (BLS). Yesterday (Monday) stock prices rebounded and erased Friday’s losses, but that jobs report is still important to understand. In this newsletter, we are going to look at what was in it, what it means for the economy, and what it might mean for markets going forward.

What was in the Jobs Report?

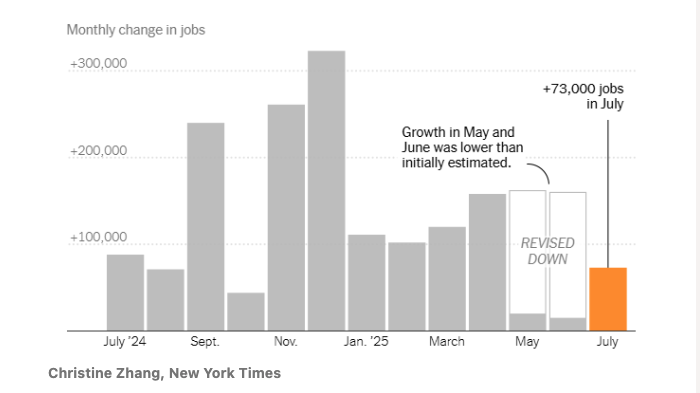

The US economy added 73,000 jobs in July which missed the consensus estimate from economists of 104,000. However, the report also contained revisions to May and June job estimates that collectively wiped out 258,000 job gains! That was the biggest downward revision since May 2020 when the US was in the depths of the COVID crisis. It means that the economy averaged just 35,000 jobs for the last three months. Most of the gains have been in health care and without those jobs the last three months would have shown a net job loss. To put these figures in perspective, the US economy created on average 186,000 jobs per month in 2024. Outside the pandemic, these recent numbers reflect the weakest job growth in the U.S. since 2011.

This isn’t good for a number of reasons. It raises the obvious question of whether steady, rapid jobs creation is over, and a new trend has emerged. Friday’s sell off was a sign that markets believed that. Monday’s rally seemed to indicate that everyone went home, thought about it and concluded that there isn’t anything to worry about. The unemployment rate is still very low by historical standards at 4.2%. Some economists have questioned that figure because they feel the participation rate is dropping due to President Trump’s immigration crackdown, but even broader measures of unemployment seem benign. For example, U4, which includes discouraged workers no longer looking for work, is still historically low at 4.5% and didn’t move at all in July.

Another bright spot in the report is that wage and workweeks increased. One of the blemishes of the otherwise bright job market over the last decade was that many people worked part-time jobs and reported not having enough hours. The jobs report could be a hint that situation is fixing itself.

Another noteworthy feature of the report is that we are starting to see signs of AI’s impact on employment. Unemployment among college graduates is up and there was a decline in staffing at business services firms. Both are being taken as hints at how AI might be weighing on employment.

While there were positives in the report, Friday’s stock market reaction indicated there were more negatives. It seems that job creation in the U.S. is slowing due to a mix of policy shifts including tariffs, immigration restrictions, demographic headwinds, automation-driven efficiency gains, and lingering economic uncertainty. Together, they’re constraining both demand for labor (employers) and supply (workers), especially in sectors that once drove broad job gains.

Just for the record, we do not put any credence in President Trump’s argument that BLS purposely manipulated the data for political purposes. Revisions to jobs data happen all the time and larger ones happen when the economy is undergoing a material shift, like when the President declares a trade war on the world. This argument is silly on its face as a negative jobs report would have been far more hurtful for the Trump administration in April or May when many of Trump’s trade negotiations were still open and investors were panicking. We’d also note that Trump has offered no evidence for his claims.

What Does it mean for the Economy?

It’s hard to look at the jobs report and see good news for the economy. Simply put, we are not creating a lot of jobs. Maybe it is the weight of tariffs on the economy. It wouldn’t surprise us if companies used tariffs as a reason to lay off people or delay hiring. Would you rush to hire if you didn’t know what your costs might look like in a month? It’s possible manufacturing jobs start to grow again as people move beyond tariffs now that they are mostly known. However, it could be that these jobs stay stagnant as companies try to digest the new costs.

Whether AI will create more jobs or cause a net loss in jobs over time is a big open question. Goldman Sachs estimates that generative AI may displace 6 to 7% of U.S. jobs over the next decade, but real peak unemployment may rise only about 0.5% thanks to job shifts. (Source: Business Insider) Tech layoffs are accelerating in 2025. Major companies like Microsoft, Intel, Google and IBM have eliminated tens of thousands of jobs, particularly in HR, support, coding and entry level white collar jobs. On the other hand new jobs are emerging. Positions like AI ethicist, ML engineer, and data strategist didn’t exist a few years ago, but are now in high demand. (Source: Financial Times). Every major technological innovation seems to come with warnings about all the jobs that will be lost and yet they typically lead to job (and wealth) creation. Remember that people warned about massive job losses resulting from the personal computer to the industrialization of factories. It’s also fun to note that the term “technological unemployment” was coined in the 1930’s by Keynes! AI may be putting downward pressure on jobs now, but that could easily turn around in the future.

Ed Yardeni, a savvy market veteran, actually thought the July jobs report was fine because he noted that people worked more hours for higher wages. Yardeni further theorized that weak payroll gains could be due to muted labor supply (lower immigration) rather than waning demand.

As with everything, time will tell us what the real answer is. Our best guess is that this deterioration is due to tariffs combined with a generally weaker job market caused by beginning phases of usable AI. Everything we hear tells us that CEO’s are attempting to put tariffs behind them now that there is more certainty about tariff rates. If that is true, hopefully these job losses are temporary, and the economy will turn back to a slow, steady upward trend. We will be watching closely to see if this jobs report was a one off or not.

What does it mean for investment markets?

We’re back in “bad news is good news” territory because the weaker data means the Fed is now likely to act sooner than later. Before these revisions, the economy looked like it was doing okay. Now it looks much more anemic and vulnerable. We’d expect the Fed to cut rates in September, especially if the next inflation report comes back relatively benign. The Wall Street Journal reports that the odds of a rate cut in September have dramatically increased from 40% to 75.5%. Reuters reports that “some estimates…put the cut probabilities closer to 92%”. Any rate cut will likely provide upside for stocks and bonds. If long-term rates start to come down, it will also benefit real estate prices. That said, we have less confidence that long-term rates will come down this time around given everything else the Trump Administration has been doing. Mortgage rates may stay high unless the Fed drops rates materially. Conversely, any continued deterioration in employment figures could send markets down, especially if the market feels like rate cuts won’t outweigh the negative effects of tariffs.

We’ve brought equity risk in most strategies back towards neutral. If the Fed moves to decrease rates and employment at least finds a floor at these levels, we will likely leave allocations alone. If the job market weakens further, we’ll likely reduce how much we have invested in stocks compared to our long-term plan. At the same time, we’ll shift more toward steadier, lower‑risk areas of the market that are more attractively priced.

Chris Roth

CIO

5T Wealth, LLC

Main (707) 224-1340

595 Coombs St

Napa, CA 94559

Disclosure and Disclaimer - Updated last on March 20, 2024 by Paul Krsek:

ELLUMINATION is the proprietary newsletter written for clients, friends, and affiliates of 5T WEALTH, LLC (5T), which is an SEC registered investment advisor. Information presented is for educational purposes only. The information does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and are not guaranteed. 5T has reasonable belief that this letter does not include any false or material misleading statements or omissions of facts regarding services or investments. 5T has reasonable belief that the content as a whole will not cause an untrue or misleading implication regarding the adviser’s services, investments, or client experiences.

The opinions expressed are those of the author and are subject to change without notice. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Any opinions, projections, or forward-looking statements expressed herein are solely those of the author. They may differ from the views or opinions expressed by other areas of 5T and are only for general informational purposes as of the date indicated.

5T has presented information in a fair and balanced manner. 5T is not giving tax, legal, or accounting advice.

Past performance should not be considered an indicator of potential future performance. If you do not consider yourself suitable, either emotionally or financially, to experience volatility and/or losses in financial markets, you should not invest. The portfolio managers at 5T do not guarantee investment results.

Charts, displays and graphs may be used as illustrations. They are not intended to be used by themselves to determine which securities to buy or sell, or when to buy or sell them. Such charts and graphs offer limited information and can’t be used on their own to make investment decisions.

ELLUMINATION does not represent the opinions of Fidelity, Fidelity Institutional Brokerage Group, NFS or anyone employed by Fidelity in any capacity. Neither Fidelity, Fidelity Institutional Brokerage Group, nor NFS, nor anyone employed by Fidelity in any capacity has participated in the creation of ELLUMINATION and they are not responsible for the contents or distribution of ELLUMINATION.

ELLUMINATION does not represent the opinions of Charles Schwab Corporation, Schwab Advisor Services or anyone employed by Schwab in any capacity. Neither Charles Schwab Corporation nor Schwab Advisor Services, nor anyone employed by Schwab in any capacity has participated in the creation of ELLUMINATION and they are not responsible for the contents or distribution of ELLUMINATION.

The investment objectives of various strategies mentioned in ELLUMINATION may be substantially different from one another. Therefore topics or investments mentioned in ELLUMINATION may or may not apply to specific managed accounts and/or strategies. If you are unsure which strategies your accounts are invested in please ask a representative of 5T to clarify that for you.

The assets held in managed accounts at 5T may include stocks, bonds, cash, commodities, foreign exchange, mutual funds or exchange traded funds (ETF's), money market accounts or limited partnerships that represent the same. They are subject to market fluctuation and the potential for losses. The assets are not insured. The value and income produced by these investment products may fluctuate, so that an investor may get back less than they initially invested.